What is behind increased rates of upfront payment of fees and student contributions?

It's been a while - seven years - since I took a look at higher education student decisions to take out a HELP loan or pay upfront. Since then we've had instability in upfront student contribution payment incentives and increased student debt salience, triggered by high-CPI indexation. Anecdotally some students paid upfront to avoid high indexation of the subsequent debt.

Student contributions & HECS-HELP

The direct incentive to pay student contributions upfront has been framed as a discount. If the upfront discount was 10% and the fee was $1,000 a person who paid upfront would incur a debt of $900. The Commonwealth compensated the university for the lost $100, but avoided holding debt that might go bad and paying interest on its own borrowings to finance lending the student $1,000. In recent years, according to estimates in the Budget papers, about 15% of each year's lending is not expected to be repaid.

The size of the incentive to pay student contributions upfront has varied over the last 20 years. Any incentive was abolished in 2017, restored for 2021 and 2022 to get Pauline Hanson to vote for Job-ready Graduates, and then abolished again from 2023.

I am in the no upfront discount camp, as I believe most people who pay upfront will do so anyway, whether there is a discount or not.

Assessing behavioural responses to the discount

The government has, in varying but limited degrees of detail, published information on the status of borrowers.

Permanent residents and some New Zealand citizens are ineligible for the discount and must pay upfront. Changes in these populations can therefore alter the overall results. These groups are discussed below.

The government has only distinguished borrowers who were eligible for HELP when the discount applies. Before the discount was first abolished in 2017 the share of eligible borrowers paying upfront was at a record low of 9.5%. We don't know the borrowing habits of this group in the years 2017-2020 but, when the discount was restored in 2021, 9.2% of eligible borrowers made an upfront payment - a move in the opposite direction of the policy intent behind restoring a discount.

In the aggregate figures, however, we can see higher rates of paying upfront after 2019. The rate went from an all-time low of 11.1% in 2019 to about 13% in each of 2022 and 2023. This is the first upward trend since the current iteration of the student loan scheme was put in place in 2005.

Students who are not eligible for a loan

Is the general upward trend after 2019 due to more permanent resident and New Zealand students who are ineligible for a HELP loan? Unfortunately the available data does not distinguish between New Zealanders who are eligible for HELP and those who are not. Nor does it distinguish between CSP and full-fee students.

The combined PR + NZ group does increase in the relevant time period (chart below), going from 4.6% in 2017 to 4.9% in 2019 and 5.3% in 2023. So this is probably a key factor in increased upfront payment, although due to data limitations it is hard to say by exactly how much.

An aside: I expect a downward trend in the NZ numbers due the Australian citizenship fast track that took effect on 1 July 2023. That will push up borrowing levels in coming years.

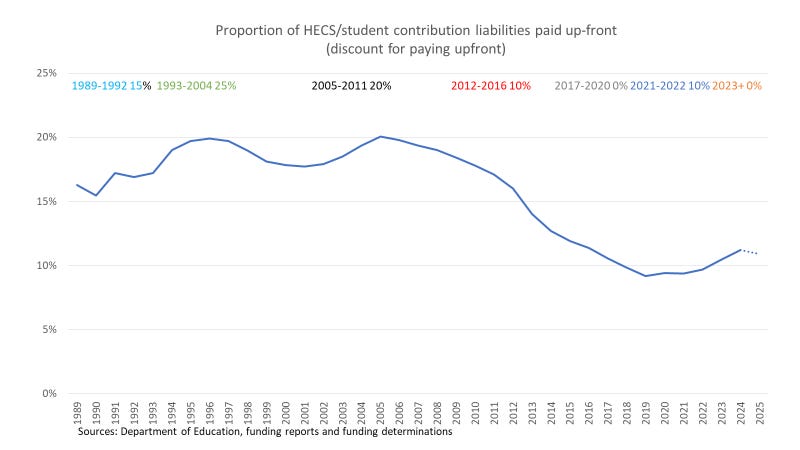

Share of student contribution liabilities paid upfront

The next analysis shifts from students to dollars. The share of students who make an upfront payment is persistently larger than the share of student contribution liabilities paid upfront. In 2023 13% of students made an upfront payment, but they paid only 10.5% of total student contribution liabilities.

As with the all-persons headcount 2019 was, at 9.2%, the all-time low share of student contributions paid upfront. It then increases to a recent peak of 11.2% in 2024. The 2025 estimate is 10.9%. As with the headcount analysis, these figures are low by historical standards but partly reverse a long downward trend.

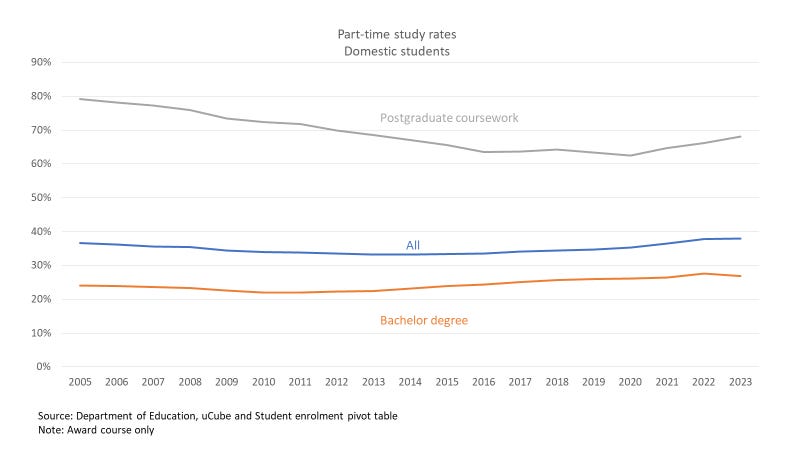

One reason for differences between persons paying and dollars paid rates is that some students only partially pay upfront. Part-time students combining study and work also help explain the differences between headcount and $$$ upfront shares. Compared to a school leaver studying full-time, part-time students have lower student contribution charges and more capacity to pay upfront. I can't neatly separate out CSP and full-fee students in the available enrolment data, but part-time study has increased in recent years.

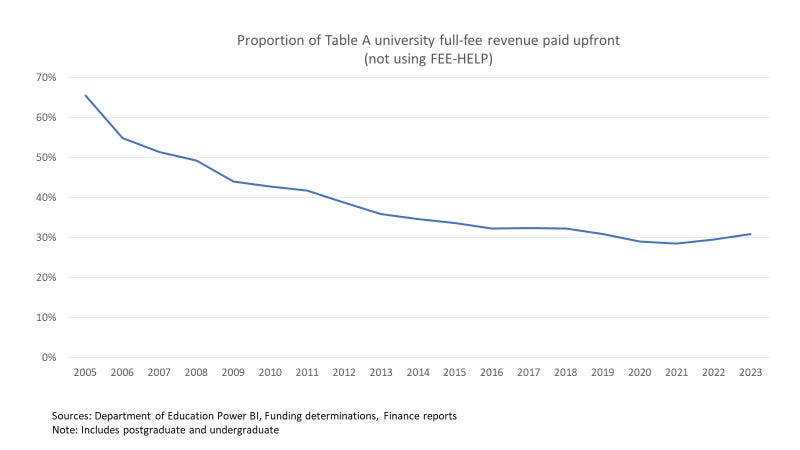

Full-fee students

For full-fee students who are supported by FEE-HELP we see the same general pattern as for CSPs - a long-term decline in the rate of paying upfront followed by a slight recovery in recent years. Changes in part-time study rates for postgraduates (the main users of FEE-HELP) are likely to be a factor in both trends.

Fortunately for HELP's finances, full-fee students pay a much larger share of their fees upfront than CSPs - around 30% instead of around 10%. For full-time employed students in postgraduate career advancement courses taking on HELP debt may not make sense. Entering the repayment system on a high income could mean an additional PAYG payment that exceeds the value of the HELP loan.

Conclusion

I don't see any reason in recent data to change my 2018 view that upfront discounts, such as those that applied in 2021 and 2022, are not cost-effective ways of reducing borrowing. While overall upfront payment rates increased after 2019, it is not clearly showing for eligible borrowers in the one year with data, 2021. It recorded a slightly lower rate than in 2016, the most recent previous year in which the discount applied.

My alternative hypothesis is that recent increases in upfront payments are mainly due to changes in the student population - more part-time students and more students who are ineligible to borrow.

While high indexation may have encouraged some students to pay fees or student contributions upfront, this will be an ephemeral effect as indexation has come back down again.

Discounts for upfront payments are mainly windfall gains for people who would have paid upfront anyway. As such, they are an unecessary expenditure and policymakers were right to end them.